In computer science a fork is a pretty common term. There are different types of forks. In this article we’ll tell you more about hard forks in cryptocurrencies.

You can visualize a hard fork in the world of crypto as a split from the original blockchain. Let’s look into this a little deeper.

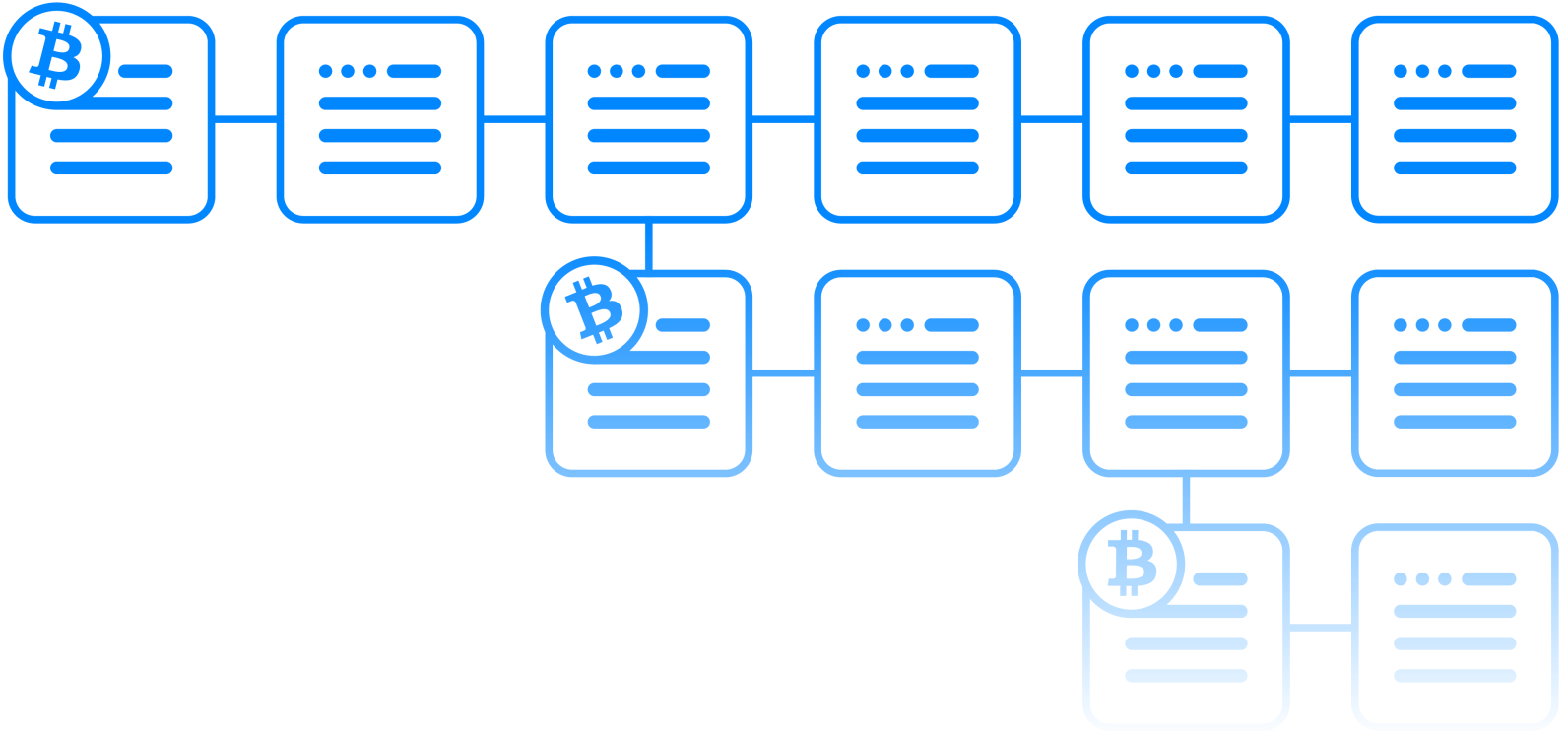

A blockchain is a ledger that keeps track of all transactions that have been done. In addition to a blockchain, coins also have a protocol in which the rules and workings are recorded.

This protocol is backed by all nodes and miners that are connected to the network. When a suggestion is done for a change in the rules, that suggestion needs to be approved by these nodes and miners.

If there is a disagreement on whether or not to implement a new set of rules, this could lead to a hard fork. In such a case, one group accepts the suggestions, so that a new protocol is formed. The group that doesn’t accept the suggestions just continue as they were doing.

But what is the real blockchain after a hard fork? Usually, most users switch to the new blockchain which means the old one slowly disappears, but that’s not always the case.

Sometimes both versions have enough support from the community which means they will coexist.

Are there any well-known hard forks?

There are many ‘famous’ hard forks, the best known ones are from Ethereum and Bitcoin.

Ethereum: The DAO hard fork

On July 20th, 2016, there was a hard fork on the Ethereum network. It’s one of the most talked about forks in the history of cryptocurrency.

The blockchain split after the DAO project was ‘hacked’. The project was a system, built on the Ethereum blockchain, that facilitated transactions.

The DAO was intended to function as a sort of venture capital fund. It was supposed to enable people from all over the world to invest in projects that were voted upon by people who contributed money. The system was built on smart contracts, but it turned out this wasn’t sufficiently secure. Through a loophole it was possible for a ‘hacker’ to transfer a total of 3.6 million Ether away from the DAO.

The term ‘hacker’ isn’t entirely correct here, since this person did not break into the system, but simply profited from poorly written code. To solve the security issue, there was a vote on a hard fork (a soft fork isn’t possible on the Ethereum network, which could be considered another problem). After a hard fork, the blockchain would refuse the DAO hack-transaction and return the tokens and ethers to the investors.

Eventually, 89 percent of the Ethereum blockchain members voted in favor of the hard fork and returning the coins.

The other share of the community (the remaining 11 percent) split from the network and continued to support the old chain. They believed ‘code is law’ and that we needed to accept the consequences of a poorly written contract. This chain, which includes the hack-transaction, is called Ethereum Classic.

Bitcoin and Bitcoin Cash

Another famous hard fork took place on August 1st, 2017. On that day the Bitcoin blockchain split in two, at block #478559. A group of developers were (and still are) in favor of changing the Bitcoin protocol. They suggested enlarging the block size from 1MB to 8MB. The idea behind this proposal was that more transactions would fit in a block this way. We won’t elaborate too much on the arguments that were given for and against the proposal, but since the community could not agree on a solution, a hard fork followed, which lead to the creation of Bitcoin Cash.

How is it decided which blockchain has the most support?

Sometimes just one chain ‘survives’ after a hard fork whilst the other chain ‘dies’. With the Bitcoin hard fork, both cryptos have enough support for Bitcoin and Bitcoin Cash to coexist.

This is because of the miners and nodes. When a majority of the miners decides to accept the new set of rules and processes them in the newly mined blocks, chances of survival are high. The next step is to get the nodes to accept these blocks as well. But even though miners and nodes represent almost the entire computing power on the network, this doesn’t mean their vote is conclusive.

The role of exchanges, brokers, and users can’t be underestimated. Keep in mind, miners have a lot of costs and they pay for them with the profits on the blocks they have mined and with the transaction fees that are in a block. But if no one is willing to purchase the coins and pay these transaction fees, miners can’t pay for their expenses. This in turn means that they’re not inclined to perform the work to sustain the blockchain.

When a hard fork takes place, do I get free coins?

If you owned bitcoin before the hard fork took place, you will automatically also own the equivalent amount in bitcoin cash. When a hard fork takes place, all private keys and the coins that come with them are copied onto the new blockchain. So if you owned bitcoin before the split and you have the private keys, you will have the same amount of bitcoin cash.

This doesn’t mean the value of your portfolio doubled though. Each coin will have its own value after the fork, based on the supply and demand of the market. Most hard forks are announced a good amount of time before they take place. Some exchanges respond to this by offering users to trade in the new coin, even before the fork takes place.

If a new coin is created through a hard fork, it depends on your wallet provider if and when you’ll be able to claim your share. It doesn’t matter if you use an online, software, or a hardware wallet; it’s always important to check with the manufacturer or software developers to see how they handle the situation.

This is even more important when you’ve stored your coins on an exchange. We always recommend to check on its website or social media to see how the exchange will deal with the fork. Will they still offer the ‘old coin’, will they offer a splitting tool, etc. A lot of exchanges will do everything in their power to accommodate to the demands of their users.

Store your coins in a hardware wallet

It’s always a good idea to store your coins in a hardware wallet, but in times of a hard fork it could be even more convenient. When a new coin gains enough support from the community, hardware wallet manufacturers like TREZOR and Ledger for example are usually the first providers to develop a splitting tool. The tool can be used to split your coin in the old one and the new one, so that you can manage both in your wallet.

Be patient

If you make a transaction in one of the first days after a fork, you could become a victim of a so-called replay attack. The best way to explain a replay attack is by using an example:

During a split, data from the old blockchain is copied to the blockchain of the new coin. If you make a transaction with coins from the new network, hackers could copy the transaction data from this transaction, and copy it to the old network.

Hackers can then use this transaction data to remove coins from your wallet. Receiving addresses are generally anonymous, so miners can’t see that it is a hacked transaction.

This problem is usually solved within a few days, by replay protection. This is an adjustment in the algorithm of the new coin, which makes a replay attack impossible.

Be careful with services provided by third parties

Services provided by third parties could be a scam. We strongly recommend to wait until your wallet provider supports the new coin, or until you can claim your coins at a reliable exchange. When in doubt, you can always contact us.

Fear of missing out?

Sign up for our weekly newsletter here!